Professionals only

setting course for fixed income

Carmignac’s fixed income team on their plans for 2020

Sponsored by

Discover more about Carmignac >

JANUARY 2020

Introduction

Welcome to another edition of SOURCE, a publication that shines the spotlight on selected funds, portfolios, and their managers…

Introduction

Welcome to another edition of SOURCE, a publication that shines the spotlight on selected funds, portfolios, and their managers.

All hands on deck

The captain behind the Carmignac fixed income team explains how her crew navigates rough markets

All hands on deck

The captain behind the Carmignac fixed income team explains how her crew navigates rough markets

Since joining Carmignac more than a decade ago, head of fixed income Rose Ouahba has been building a team of ‘passionate and hard-working people’, which is bracing for another year of challenging markets.

Carmignac has built its strong fixed income capability by hiring managers with ‘entrepreneurial spirit’, she said. By this, she means a focus on the long term and an ability to work together in a collaborative manner.

‘I want to have these people working with each other, helping each other, supporting each other. They must prove that by being together, they are stronger than being on their own, and I really encourage that type of mentality,’ Ouahba said. This approach paid off last year, which saw Ouahba take on responsibility for the firm’s flagship Carmignac Patrimoine portfolio alongside head of equities David Older, while keeping her role as head of fixed income.

The €11.7bn (£9.9bn, as at 29/11/2019) multi-asset fund had been managed by Edouard Carmignac since inception in 1989, but he handed over the reins to his co-managers to take a step back from fund management at the beginning of 2019. Ouahba now bears responsibility for the fixed income portion of the multi-asset portfolio, while Older is in charge of the equity segment.

Ouahba said it was the strength of her team that helped the transition to her new asset allocator role through the support and leadership they provide on the fixed income side. In terms of fixed income expertise, there has been continuous reinforcement in terms of size, products and resources within Carmignac. In 2007, the company had 23% of assets under management in fixed income, and that figure stood at 64% at the end of 2019.

‘I have worked with the core of the team for five years,’ she said, while also highlighting the arrival of a number of high-profile portfolio managers into the group in 2019. ‘I know them and I trust them all.’

Much-needed flexibility

The fixed income team at Carmignac consists of seven fund managers reporting to Ouahba, as well as a number of analysts supporting them with research. The investment approach follows one overarching philosophy: flexibility.

‘What we mean by this is two simple things,’ Ouahba said. ‘We are offering an asset allocation service and a risk management focus to our clients, which can involve top-down or bottom-up selection.’

This philosophy permeates each of the fixed income portfolios the firm offers. The range consists of generalist strategies with ascending levels of risk and specialised propositions.

The products with the lowest volatility, Carmignac Sécurité, invests in European bonds and is co-managed by Keith Ney and Marie-Anne Allier, who joined the group this year from Amundi.

The team has also developed an unconstrained fixed income strategy, which aims to capture better opportunities globally, remaining loyal to Carmignac’s management DNA.

‘We are offering an asset allocation service and a risk management focus to our clients, which can involve top-down or bottom-up selection’

Rose Ouahba

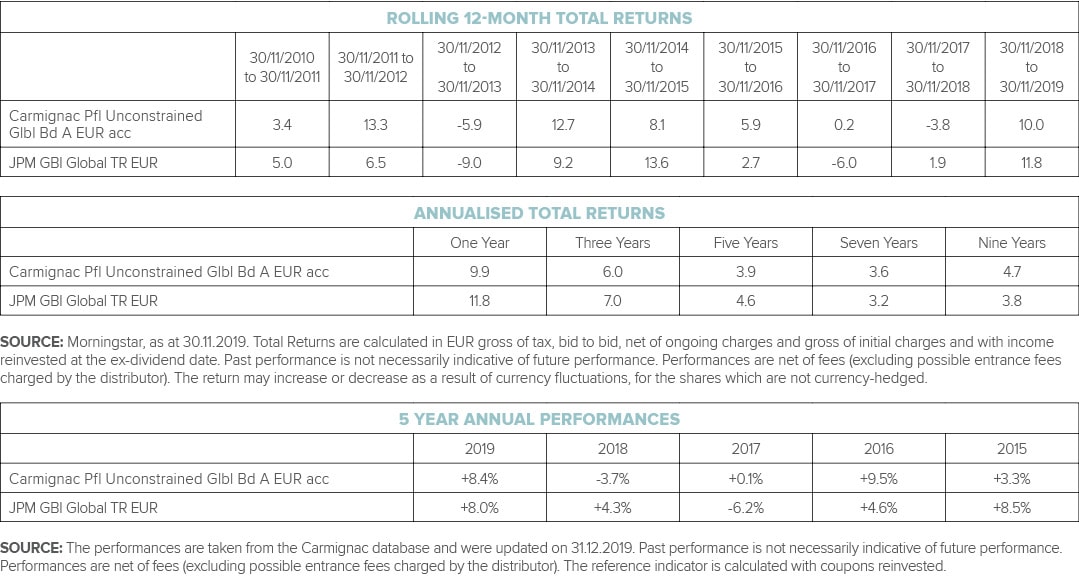

Carmignac Portfolio Unconstrained Global Bond is the highest risk product of the three generalist funds. Managed by Charles Zerah, this fund is benchmark-agnostic, globally diversified across developed and emerging markets, and contains sovereign and corporate bonds.

The newly restructured Carmignac Portfolio Unconstrained Euro Fixed Income fund sits in the middle in terms of risk. It also invests in bonds globally, but hedges the exposure back to a single currency. This fund is run by former Edmond de Rothschild Asset Management duo Guillaume Rigeade and Eliezer Ben Zimra.

Finally, the Carmignac Portfolio Unconstrained Credit fund invests solely in the credit market and is co-managed by Pierre Verlé and Alexandre Deneuville.

2020 outlook

Looking back at 2019, Ouahba said two calls generated particularly strong performance for the fixed income funds. The first was the exposure to the rally following the European Central Bank’s monetary policy easing. The second was strong stock-picking in the corporate sector, where the managers avoided the CCC-rated bonds that suffered significant falls.

The team also managed to avoid the key default risks in emerging markets coming from Argentina, Venezuela, Ecuador and Lebanon. Instead, they made contrarian investments in Turkey and Chile, which paid off.

‘In 2020, we intend to stay exposed to peripheral risk in Italy and Greece, as well as corporates,’ Ouahba said. ‘We expect to raise exposure to emerging markets once we have more clarity on the direction of the dollar.’

To balance this risk, the portfolios are long the short end of the curve in the Treasuries market and long Australian rates.

NO STRINGS ATTACHED

Bonds have had a tumultuous few years, with yields nearing record lows. To avoid being tied down by faltering benchmarks, some experts recommend going unconstrained

NO STRINGS ATTACHED

Bonds have had a tumultuous few years, with yields nearing record lows. To avoid being tied down by faltering benchmarks, some experts recommend going unconstrained

After a decade of unprecedented central bank stimulus, many are finally beginning to question the longevity of the current 35-year bull market in bonds. Debt and demographics may be weighing on growth, but central banks are beginning to question the continued efficacy of their programmes, and governments around the world are slowly beginning to embrace fiscal policies. With fixed income yields still near record lows, that leaves investors at something of a crossroads.

Cue global unconstrained bonds

‘Given the difficulties facing fixed income investors right now, it’s really quite important to be unconstrained and not tied to a specific country or benchmark,’ said Charles Zerah, manager of the €876m (as at 29/11/19) Carmignac Portfolio Unconstrained Global Bond strategy. ‘Not only if inflation rises or yields begin to turn up. But the correlation between equities and bonds has been changing of late, with bonds not always acting as that ballast or protection. At the same time, global political uncertainty is likely to continue and so, being flexible allows you to actually benefit from these changes.’

So, how exactly does Zerah, who is celebrating his 10th anniversary on the fund in March, run the fund? And with such a wide universe to choose from, how does he find alpha?

‘Being a global unconstrained fund, we do have a top-down approach based on the work of our chief economist, Raphael Gallardo, and our CIO, Edouard Carmignac,’ he said. ‘I’ll use this input, as well as the input from our other experts and analysts to look at differing regions – including both developed markets and emerging regions.’

From there, Zerah and his team have a three-step process. The first is to work out the allocation to different countries and corporates, as well as cash. ‘The cash is important for an unconstrained fund,’ he said. ‘We have the ability to hold a pretty large amount of cash or quasi cash in the fund, sometimes up to 40%, where we can make currency moves or hedge positions. That’s the first step.’

The second, he said, is to manage the duration of the securities he holds. The fund has a very flexible approach, and the duration can range from -4 to over 10, with Zerah unafraid to make big duration calls at market turning points to limit downside risks, if inflation returns or buy longer-dated, higher-convexity bonds if a recession or slowdown is on the horizon.

‘Given the difficulties facing fixed income investors right now, it’s really quite important to be unconstrained and not tied to a specific country or benchmark’

Charles Zerah

The third and final step is to use detailed analysis to pick individual securities based on issuers, issues and instruments, which is where the bottom-up approach meets their top-down views.

‘We really have a core portfolio which follows this three-step process, where we select govies [government bonds] and corporates or credit based on our allocation and macro models,’ he added. ‘From there, we’ll look to modify duration if needed, and the same is for currency allocation as well. We can use derivatives, futures on govies, swaps on rates, swaptions and even CDSs [credit default swaps] if we want to.’

And while most investors are positioning for stronger global growth and reflation in 2020, Zerah said that he remains cautious with valuations so stretched – despite the fund’s risk profile allowing him to take more risk should he see opportunity.

‘Even with a phase-one trade deal, we don’t think that this will change the face of the world,’ he said. ‘That’s why we’re relatively cautious. We’re happy to maintain longer duration while credit markets are not cheap. So, we are trying to find opportunities on specific stories and names, such as European financials. There are some good stories in EM, such as Turkey’s bonds denominated in euros or Pemex, but it’s important to remain flexible and not be tied down to a certain region or duration.’

Bolstering the team

The increasing need for more flexible fixed income approaches is one of the main reasons Carmignac has been working to bolster its unconstrained team. This includes rebranding the Carmignac Portfolio Capital Plus fund as the Carmignac Portfolio Unconstrained Euro Fixed Income fund in September 2019, although the unconstrained approach remains in line with Carmignac’s 30-year style.

Formerly the Carmignac Portfolio Capital Plus fund, it was recently rebranded as the Carmignac Portfolio Unconstrained Euro Fixed Income fund, with two former star Rothschild managers, Guillaume Rigeade and Eliezer Ben Zimra, taking the reins in July.

‘We jumped at the opportunity,’ Rigeade said. ‘Carmignac is a famous asset management company, but it’s also a company that is very focussed on asset management.

‘We benefit from the firm’s big investment network, with an economist, central bank watcher, many different managers and analysts all helping us to make the best top-down and bottom-up calls.’

A slightly less risky version of the Global Unconstrained fund, the duo invest in global fixed income markets. Non-euro-denominated investments will systematically be hedged back into the euro, hence the fund’s name.

Their top-down, bottom-up approach is well suited to the fixed income team within Carmignac, which now numbers 13 people under the leadership of Rose Ouahba.

The Carmignac Porftolio Unconstrained Euro Fixed Income fund takes a dynamic approach when investing, with allocation to various fixed income markets, active and flexible management of duration, and single security selection of issuers, issues and instruments.

‘The volatility of this fund is relatively low, at around 3% to 5%,’ Ben Zimra said. ‘But that doesn’t mean we can’t find great opportunities. Like Charles, we see the global economy growing at below-trend growth, particularly in developed countries, while central banks should remain very accommodative.

‘We actually think some yields could drop again – it’s very possible,’ he added. ‘We continue to build exposure in Europe and have a long exposure to the short-end of the US market, where we think the US Federal Reserve will continue to drop rates and become more accommodative next year. We actually have positive duration on the US yield curve, and we think that the Fed will try to steepen the curve.

‘The fund is also long on Mexico, Russia and China, where yield curves rates should benefit from easier monetary policies from central banks because of still elevated real rates. And, perhaps from a contrarian angle, we are long Canada and Norway – two countries where central banks have tightened. But we think this is unjustified and they’ll have to reverse course soon. And, like Charles, we like European financials, which are now better capped but still pay a healthy yield.’

Exploiting Credit opportunities

Carmignac’s Pierre Verlé and Alexandre Deneuville tell us about their idiosyncratic approach

exploiting credit opportunities

Carmignac’s Pierre Verlé and Alexandre Deneuville tell us about their idiosyncratic approach

The current overall picture of tighter credit spreads masks a wide dispersion at a security-specific level, said Alexandre Deneuville, co-fund manager of Carmignac Portfolio Unconstrained Credit. In today’s environment, growing investor fear is combined with negative yields on risk free assets: as a result, those bonds the wider market considers relatively safe are pricier than ever, while those perceived as riskier can face a swift de-rating. This type of dispersion is exactly what bond pickers need to find opportunities, he added.

‘Our conviction-driven and non-benchmarked approach gives us the ability to range across the entire credit spectrum and exploit opportunities we find at bond level for good risk-adjusted returns,’ he said. Nevertheless, he describes the current fund positioning as ‘prudent’ given the backdrop of expensive markets, an extended credit cycle and evidence of excess in both investment grade and high yield: ‘At a company level, we are seeing many cases of too much leverage and decreasing investor protection,’ he said.

‘Our conviction-driven and non-benchmarked approach gives us the ability to range across the entire credit spectrum’

Alexandre Deneuville

The fund can have up to 50% in high yield and currently has just under 45% gross, but net of hedges the figure is 28%, while emerging markets, which can go up to 25%, is 21.6% gross and 16.1% net. At a total 73% net, exposure is at the lower range of what it has been over the fund’s two-and-a-half year lifespan; but despite this fairly low exposure, the fund remains well diversified, with over 100 positions.

The ability to manage exposure is a key part of the fund’s philosophy, said Pierre Verlé, head of credit at Carmignac and co-fund manager of Carmignac Portfolio Unconstrained Credit. ‘A lot of funds in the market are over-constrained by having a target return. Because they aim to achieve a constant return at every point of the cycle, the risk exposure has to vary depending on how easy it is to achieve that target in a given environment,’ he said.

The reality is that the more expensive markets are, the more risk these funds will be forced to take to meet their targets, Verlé said. This is why Carmignac takes the opposite approach, he added.

The Carmignac process is based on the managers’ assessment of the market environment, based not only on indices but also value evident in primary and secondary markets, general investor behaviours and risk appetite.

‘When we consider the market to be cheap with a lot of excellent risk/reward situations available, we will be aggressive; conversely, when markets are expensive – as they are today – we will be prudent and run a low net exposure while we try to “hide” in idiosyncratic positions,’ Verlé said.

As a result, during times when risk is cheap, the fund can be more volatile than its peers; the flipside is that during expensive periods, it can have lower volatility than its peers.

SECTOR

OVERVIEW:

Mixed Asset

frank talbot

Head of Investment Research, CITYWIRE

SECTOR OVERVIEW:

Mixed Asset

frank talbot

Head of Investment Research, CITYWIRE

Since Zerah began management of Carmignac‘s Unconstrained Global Bond nearly a decade ago, he has outpaced the global government bond index; delivering gains of 58.3% to his investors while the market has risen 51.7%.

SOURCE: Morningstar, TR% Growth EUR, as at 30.11.2019. Performance is based on total return in EUR calculated gross of tax, bid to bid, ignoring the effect of initial charges and with income reinvested at the ex-dividend date.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The return may increase or decrease as a result of currency fluctuations, for the shares which are not currency-hedged.

The reference indicator is calculated with coupons reinvested.

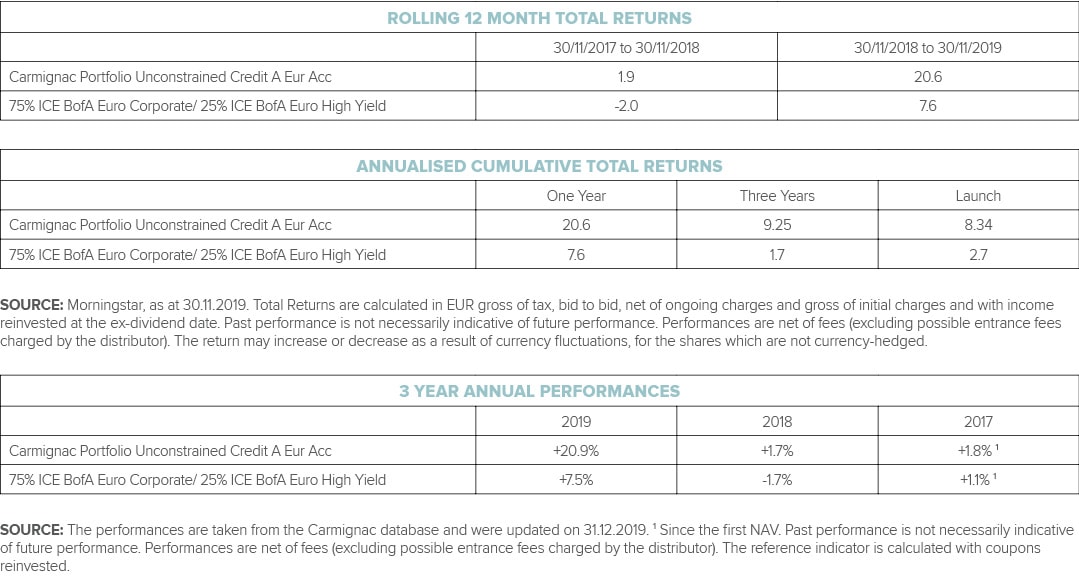

The team of Pierre Verlé and Alexandre Deneuville enjoyed an excellent start to their management of the Global Unconstrained credit fund, returning 24.4% in less than two and half years, significantly ahead of the 75% ICE BofA Euro Corporate/ 25% ICE BofA Euro High Yield reference indicator’s 6.6% rise.

SOURCE: Morningstar, as at 30.11.2019. Performance is based on total return in EUR calculated gross of tax, bid to bid, ignoring the effect of initial charges and with income reinvested at the ex-dividend date. Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The return may increase or decrease as a result of currency fluctuations, for the shares which are not currency-hedged. The reference indicator is calculated with coupons reinvested.

Since Ney joined the portfolio at the beginning of January 2013 he has comfortably outperformed both the average manager and the reference indicator; with his returns of 7.4% close to double the indexes 4.2% and average manager’s 4.5% gains.

SOURCE: Citywire Discovery/Lipper, as at 30.11.2019. Performance is based on total return in EUR calculated gross of tax, bid to bid, ignoring the effect of initial charges and with income reinvested at the ex-dividend date. Average manager is the based upon the managers tracked globally in Citywire’s Bonds – Euro Short Term peer group. Contributing performance Carmignac Securite A EUR Acc (Jan’13 – Present) and Carmignac Pfl Securite F CHF acc Hdg (Jan’13 – Present). Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The return may increase or decrease as a result of currency fluctuations, for the shares which are not currency-hedged.

Keith Ney is top quartile on a risk-adjusted basis over both one and five years in the Bonds – Euro Short Term peer group globally. This can be seen by his position in the upper right hand quadrant of the graph. This position justifies the market share of leading assets that Ney and co-manager Marie-Anne Allier run in the peer group.

SOURCE: Citywire Discovery, as at 31.10.2019. Risk-adjusted percentiles are calculated in EUR gross of tax, bid to bid, ignoring the effect of initial charges and with income reinvested at the ex-dividend date. Peer group rankings are based on managers tracked by Citywire in the UK. Market share data based on total assets under management by managers tracked globally in Citywire’s Bonds – Euro Short Term peer group.

Fishing for fixed income value in turbulent waters

The Carmignac Sécurité fund team explains their investment strategy and how it has paid off after a year of volatility

Fishing for fixed income value in turbulent waters

The Carmignac Sécurité fund team explains their investment strategy and how it has paid off after a year of volatility

Fixed income has been somewhat troublesome in today’s seemingly perpetual low interest-rate environment. Flat yields and low growth have made it hard to extract value, but with new co-fund manager Marie-Anne Allier joining Keith Ney in April 2019, the Carmignac Sécurité fund expects returns to rally in 2020.

Allier has extensive experience in European fixed income aggregate fund management. She joined the firm from Amundi where she had been the head of euro fixed income management since 2010. Allier has also held senior fixed income management roles at SG Asset Management and GTI Finance.

Ney, meanwhile, has managed Carmignac Sécurité since 2013, initially as co-manager and then as sole manager from 2014. He was previously head of credit for the firm.

With a 30-year track record, Sécurité is high profile within the investment world and has formed a key element of Carmignac’s fixed income offering since the company was founded in 1989. Positive performance is, therefore, key — not just for investors, but also for the brand’s reputation.

‘For the past 20 years, all fixed income managers have begun the year saying how hard it is to extract value, and in 2019 we’ve done just that. 2020 is a new year and we want to be having the same positive discussion this time next year,’ Allier said.

Indeed, the fund has taken advantage of three factors in 2019 to produce a return of 3.57% compared with a reference indicator performance of 0.07%. ‘At the start of the year, we felt that the US and China had both over-tightened and that the European Central Bank was behind the curve,’ Ney explained.

He and Allier took the view that curves were steep but would flatten, that interest rates would depress further and that credit spreads would compress.

‘For the past 20 years, all fixed income managers have begun the year saying how hard it is to extract value, and in

2019 we’ve done just that’

Keith Ney

‘Those views have given us strong performance,’ Ney said. ‘In addition, we have realised some gains, reduced our duration risk and then positioned the portfolio for a bounce in yields,’ he said.

Allier added that reducing exposure to Italy, Spain and France over the summer did lead to increased cash holdings, but that the fund then looked to increase holdings in short-term, high-rated credit where appropriate.

‘We prefer to have some cash on hand rather than invest in something we consider too risky, but obviously, we also want to invest,’ Allier said.

Partnership

Good performance in 2019 has been the first benefit of this new partnership. The pair said the approach was very much a joint one.

‘We don’t divide the workload in two – rather, we use our different backgrounds and experiences to look at the same thing from two viewpoints,’ she said.

Ney agreed: ‘We have a partnership approach and are generally in sync when it comes to macro views. In an environment of regulatory and financial repression, we work together to get those small pockets of value. This also helps to minimise the risk,’ he said.

Both are also keen to emphasise the reinforced expertise that comes from having a tight-knit fixed income team. Indeed, it has been boosted with the arrival of credit and euro fixed income analysts, strengthening bottom-up expertise.

In terms of the macro outlook, the fact remains that positive performances are hard to come by in a negative-yield environment. Indeed, now in the fifth year of the negative interest-rate experiment, there has been concern that manufacturing weakness could spread to services. In addition, inflation has been well below the mandate, and synchronised easing of monetary policy has now been halted. In terms of fiscal policy, pressure is mounting to extend the cycle, even though this is deemed unlikely to happen in the short term.

‘We expect to stay within a low-yield environment for at least the next six to eight months unless we see significant growth in either Europe or the US,’ Allier said. ‘While committed to respect our average investment grade limit, we can exploit opportunities across markets,’

she said.

This is just the latest in a difficult few years for the asset class, and the fund itself took a hit in 2018, the first in its long history. According to Ney, this was due to underestimating the impact of Italy’s political situation on German bunds in May 2018 and then overestimating the extent to which bunds would stabilise in Q4.

‘Our strong convictions are backed by high-rated, low-duration, low-risk investments’

Marie-Anne Allier

Nevertheless, the quest continues. Allier explained the fund’s strategy in this tricky environment: ‘We look for high-rated, low-duration, low-risk investments that allow for conviction and performance,’ she said.

She said the fund is taking short-term positions and needs to have the conviction to back those, with 50% of allocation falling into this bracket and a further 10% within a high-conviction credit environment numbering around five names. The remainder, she said, is invested in government bonds, ‘mainly Greece, Cyprus and Austria’.

‘We like a story that has spreads that have done well and reduced our overall risk,’ she said.

The strategy has also been able to carry and spread compression potential in short-maturity credit markets as well as look hard at long special idiosyncratic situations such as Altice, Eurofins, Pemex and Teva. Directional convictions on Greece and Italy as well as semi-core and Cyprus long-end relative value strategies have also come into play. The team also thinks that European CLOs are a great carry for credit quality.

Be bold

Both managers agree that although it is important to minimise risk and conviction, the fund should also be courageous and take positions, as mandated.

‘The fund is essentially a flexible, low-duration fund mainly invested in euro denominated debt with a wide duration risk of between -3 and +4,’ Ney said.

He explained that Sécurité is unique in that it can allocate duration risk wherever the managers see fit – whether they see value on a curve, in a particular country or within government or corporate bonds. Risk management framework is disciplined through a maximum of 20% non-euro credit and maximum of 10% non-euro FX. High-yield exposure has a maximum of 10% for government bonds and 10% for corporate bonds.

‘We are lucky in that we are not constrained as long as we stick to the remit of European investment grade and above bonds. This flexibility means we can continue to do well in an environment of financial repression,’ Ney said.

MAIN RISKS OF THE FUNDS

MAIN RISKS OF THE FUNDS

CARMIGNAC PORTFOLIO UNCONSTRAINED GLOBAL BOND

CREDIT: Credit risk is the risk that the issuer may default. INTEREST RATE: Interest rate risk results in a decline in the net asset value in the event of changes in interest rates. CURRENCY: Currency risk is linked to exposure to a currency other than the Fund’s valuation currency, either through direct investment or the use of forward financial instruments. DISCRETIONARY MANAGEMENT: Anticipations of financial market changes made by the Management Company have a direct effect on the Fund‘s performance, which depends on the stocks selected.

CARMIGNAC PORTFOLIO UNCONSTRAINED EURO FIXED INCOME

INTEREST RATE: Interest rate risk results in a decline in the net asset value in the event of changes in interest rates. CREDIT: Credit risk is the risk that the issuer may default. CURRENCY: Currency risk is linked to exposure to a currency other than the Fund’s valuation currency, either through direct investment or the use of forward financial instruments. EQUITY: The Fund may be affected by stock price variations, the scale of which is dependent on external factors, stock trading volumes or market capitalization.

CARMIGNAC PORTFOLIO UNCONSTRAINED CREDIT

CREDIT: Credit risk is the risk that the issuer may default. INTEREST RATE: Interest rate risk results in a decline in the net asset value in the event of changes in interest rates. LIQUIDITY: Temporary market distortions may have an impact on the pricing conditions under which the Fund might be caused to liquidate, initiate or modify its positions. DISCRETIONARY MANAGEMENT: Anticipations of financial market changes made by the Management Company have a direct effect on the Fund‘s performance, which depends on the stocks selected.

CARMIGNAC SÉCURITÉ

INTEREST RATE: Interest rate risk results in a decline in the net asset value in the event of changes in interest rates. CREDIT: Credit risk is the risk that the issuer may default. RISK OF CAPITAL LOSS: The portfolio does not guarantee or protect the capital invested. Capital loss occurs when a unit is sold at a lower price than that paid at the time of purchase. CURRENCY: Currency risk is linked to exposure to a currency other than the Fund’s valuation currency, either through direct investment or the use of forward financial instruments.

The funds present a risk of loss of capital.

*For the A Eur Acc share classes. Risk Scale from the KIID (Key Investor Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time.

CITYWIRE INVESTMENT WARNING

This communication is by Citywire Financial Publishers Ltd (“Citywire”) and is provided in Citywire’s capacity as financial journalists for general information and news purposes only. It is not (and is not intended to be) any form of advice, recommendation, representation, endorsement or arrangement by Citywire or an invitation to invest or an offer to buy, sell, underwrite or subscribe for any particular investment. In particular, the information provided will not address your particular circumstances, objectives and attitude towards risk.

Any opinions expressed by Citywire or its staff do not constitute a personal recommendation to you to buy, sell, underwrite or subscribe for any particular investment and should not be relied upon when making (or refraining from making) any investment decisions. In particular, the information and opinions provided by Citywire do not take into account your personal circumstances, objectives and attitude towards risk.

Citywire uses information obtained primarily from sources believed to be reliable (such as company reports and financial reporting services) however Citywire cannot guarantee the accuracy of information provided, or that the information will be up-to-date or free from errors. Investors and prospective investors should not rely on any information or data provided by Citywire but should satisfy themselves of the accuracy and timeliness of any information or data before engaging in any investment activity. If in doubt about a particular investment decision an investor should consult a regulated investment advisor who specialises in that particular sector.

Information includes but is not restricted to any video, article or guide content created or provided by Citywire.

For your information we would like to draw your attention to the following general investment warnings:

The price of shares and investments and the income associated with them can go down as well as up, and investors may not get back the amount they invested. The spread between the bid and offer prices of securities can be significant in volatile market conditions, especially for smaller companies. Realisation of small investments may be relatively costly. Some investments are not suitable for unsophisticated or non-professional investors. Appropriate independent advice should be obtained before making any such decision to buy, sell, underwrite or subscribe for any investment and should take into account your circumstances and attitude to risk.

Past performance is not necessarily a guide to future performance. Citywire Financial Publishers Ltd. is authorised and regulated by the Financial Conduct Authority (no: 222178).

TERMS OF SERVICE

Citywire Source is owned and operated by Citywire Financial Publishers Ltd (“Citywire”). Citywire is a company registered in England and Wales (company number 3828440), with registered office at 1st Floor, 87 Vauxhall Walk, London, SE11 5HJ and is authorised and regulated by the Financial Conduct Authority (no: 222178) to provide investment advice and is bound by its rules.

1. Intellectual Property Rights 1.1 We are the owner or licensee of all copyright, trademarks and other intellectual property rights in and to these works (including all information, data and graphics in them) (collectively referred to as “Content”). You acknowledge and agree that all copyright, trademarks and other intellectual property rights in this Content shall remain at all times vested in Citywire and /or its licensors. 1.2 This Content is protected by copyright laws and treaties around the world. All such rights are reserved. Images and videos used on our websites are © iStockphoto, Alamy, Thinkstock, Topfoto, Getty Images or Rex Features (among others). For credit information relating to specific images where not stated, please contact picturedesk@citywire.co.uk. 1.3 You must not copy, reproduce, modify, create derivative works from, transmit, distribute, publish, summarise, adapt, paraphrase or otherwise publicly display any Content without the specific written consent of a director of Citywire. This includes, but is not limited to, the use of Citywire content for any form of news aggregation service or for inclusion in services which summarise articles, the copying of any Fund manager data (career histories, profile, ratings, rankings etc) either manually or by automated means (“scraping”). Under no circumstance is Citywire content to be used in any commercial service.

2. Non-reliance 2.1 You agree that you are responsible for your own investment decisions and that you are responsible for assessing the suitability and accuracy of all information and for obtaining your own advice thereon. You recognise that any information given in this Content is not related to your particular circumstances. Circumstances vary and you should seek your own advice on the suitability to them of any investment or investment technique that may be mentioned. 2.2 The Fund manager performance analyses and ratings provided in this Content are the opinions of Citywire as at the date they are expressed and are not recommendations to purchase, hold or sell any investment or to make any investment decisions. Citywire’s opinions and analyses do not address the suitability of any investment for any specific purposes or requirements and should not be relied upon as the basis for any investment decision. 2.3 Persons who do not have professional experience in participating in unregulated collective investment schemes should not rely on material relating to such schemes. 2.4 Past performance of investments is not necessarily a guide to future performance. Prices of investments may fall as well as rise.

2.5 Persons associated with or employed by Citywire may hold positions or take positions in investments referred to in this publication. 2.6 Citywire Financial Publishers Ltd operate a policy of independence in relation to matters where the operators may have a material interest or conflict of interest.

3. Limited Warranty 3.1 Neither Citywire nor its employees assume any responsibility or liability for the accuracy or completeness of the information contained on our site. 3.2 You acknowledge and agree that any information that you receive through use of the site is provided “as is” and “as available” basis without representation or endorsement of any kind and is obtained at your own risk. 3.3 To the maximum extent permitted by law, Citywire excludes all representations, warranties, conditions or other terms, whether express or implied (by statute, common law, collaterally or otherwise) in relation to the site or otherwise in relation to any Content or Feed, including without limitation as to satisfactory quality, fitness for particular purpose, non-infringement, compatibility, accuracy, or completeness. 3.4 Notwithstanding any other provision in these Terms, nothing herein shall limit your rights as a consumer under English law.

4. Limitation of Liability To the maximum extent permitted by law, Citywire will not be liable in contract, tort (including negligence) or otherwise for any liability, damage or loss (whether direct, indirect, consequential, special or otherwise) incurred or suffered by you or any third party in connection with this Content, or in connection with the use, or results of the use of Content. Citywire does not limit liability for fraudulent misrepresentation or for death or personal injury arising from Citywire’s negligence.

5. Jurisdiction These Terms are governed by and shall be construed in accordance with the laws of England and the English courts shall have exclusive jurisdiction in the event of any dispute in connection with this Content or these Terms.