VALUE AS

A VIRTUE

Presenting the Macquarie ValueInvest Global Equity Strategy

Sponsored and paid for by

OCTOBER 2019

INTRODUCTION

Welcome to another edition of SOURCE, a publication that shines the spotlight on selected funds, portfolios, and their managers. This time it’s the turn of Macquarie’s ValueInvest Global Equities Team with an in-depth profile and Q&A with Portfolio Managers Jens Hansen and Klaus Petersen, plus supporting analysis from Citywire.

INTRODUCTION

Welcome to another edition of SOURCE, a publication that shines the spotlight on selected funds, portfolios, and their managers. This time it’s the turn of Macquarie’s ValueInvest Global Equities Team with an in-depth profile and Q&A with Portfolio Managers Jens Hansen and Klaus Petersen, plus supporting analysis from Citywire.

Jens Hansen

& Klaus

Petersen

PROFILE

Jens Hansen

& Klaus

Petersen

PROFILE

How to stay invested:

go global and play defensive

How to stay invested:

go global and play defensive

tocks may have enjoyed a strong first half of 2019, but there is no shortage of risks on the horizon and equity investors are understandably becoming more cautious. Yet without any clear signs of a major recession, and with central banks turning more accommodative of late, divesting completely from stocks seems premature. So, what is an investor to do?

Stocks may have enjoyed a strong first half of 2019, but there is no shortage of risks on the horizon and equity investors are understandably becoming more cautious. Yet without any clear signs of a major recession, and with central banks turning more accommodative of late, divesting completely from stocks seems premature. So, what is an investor to do?

One solution might be to invest in a defensively-minded global fund, such as the Macquarie ValueInvest Global Equity Fund (the Fund), which was launched in 2001 and seeks to capture significant upside while simultaneously reducing downside risk. The Macquarie ValueInvest Global Equity Strategy (the Strategy) has a strong long-term track record having been launched in 1998, and seeks to balance valuation and quality to reduce its exposure to risks.

‘At this point in the cycle, it makes sense to have a sharper focus on valuation,’ explained portfolio manager Jens Hansen, who has spent over 17 years with the Luxembourg-based ValueInvest team and also serves as CIO. ‘Investors continue to pile into passives at the expense of active, often paying little attention to valuation or quality. This isn’t a wise strategy in the long-term.’

VALUE AND PATIENCE – THE ADVANTAGES OF A ‘BORING’ APPROACH

With central banks adding unprecedented levels of liquidity and global yield curves flattening, value investing – the most tried and tested of all investment philosophies – has struggled in recent years. The Morgan Stanley Capital International (MSCI) World Value Index (the Index), for example, has largely been left for dead by its growth counterpart over one, three, five and 10-years, with investors shunning financials, energy and industrials for trendy tech and consumer names.

But this does not mean that value can’t outperform, said Hansen, who insists that a modern value approach shouldn’t simply entail focusing on metrics such as price-to-earnings or price-to-book, which have dragged down the aforementioned value Index.

‘We call ourselves value investors, but we don’t just focus on buying cheap companies. These companies can often be cheap for a reason, and typically struggle to earn a decent return on investment,’ he noted. ‘Instead, we’re patient long-term investors, looking for businesses that we believe can compound value over time. As such, closely examining their quality and understanding how they create value are just as important as paying below what we think is fair value.’

‘We’re patient long-term investors, looking for businesses that we believe can compound value over time’

JENS HANSEN

And the team are happy to explain that a ‘boring’ approach focused on discipline, consistency and simplicity has been the main driver of their results.

‘We don’t believe we have a major informational edge when it comes to stock selection,’ Hansen’s colleague and long-time co-portfolio manager, Klaus Petersen, admitted. ‘What we do have is a disciplined and consistent investment process that we’ve used successfully for 20 years. Our approach enables us to take a long-term view on the value of a business, and our embedded investment rules help to reduce the risk of mistakes – which is paramount in compounding wealth.’

‘Investing is not necessarily exciting, and rather akin to running a marathon. We aim to benefit from short-term bias and volatility, which simply means that companies – especially less fashionable names – can be bought for less than their fair value at times based on near-term mispricings. From there, it’s difficult to be patient and wait – sometimes years – for those companies to grow into their fair value. They can have a high return on capital, but long-term value creation does require perseverance.’

PLAYING DEFENSIVE – WHY EARNINGS STABILITY IS KEY

What does the portfolio look like, then? And how does the team go about managing risks through the cycle?

‘The portfolio reflects our systematic, bottom-up investment process,’ said Hansen. ‘We take a deep dive into a company’s earnings stability, return on invested capital, growth potential, and financial leverage,’ he added. ‘It’s by focusing on these key pillars – earnings stability in particular – that allow us to evaluate companies depending on their risk premium.’

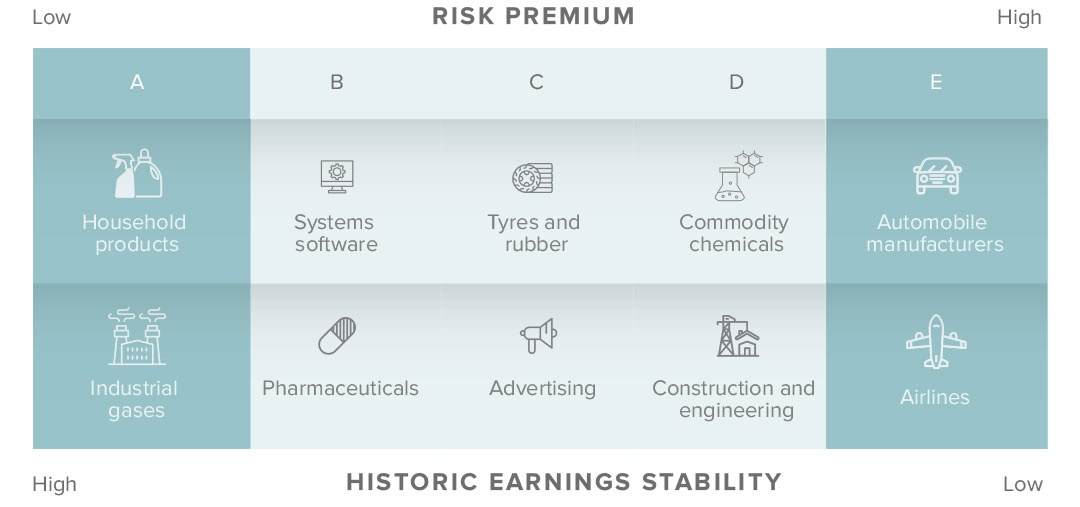

‘What makes our investment process unique is the way we assign risk premiums,’ explained Petersen. ‘We see ourselves as business owners, concerned with the volatility of operating earnings rather than swings in the stock price. Our proprietary investment system divides the global investment universe into five different risk categories (A – E); with category ‘A’ having the highest historic earnings stability, and category ‘E’ the lowest. High earnings stability translates to a low risk premium, and vice versa for low earnings stability.’

Industries like household products or industrial gases, for example, have historically exhibited highly visible and stable earnings, and as such have received an ‘A’ risk category rating, according to their system. By contrast, industries such as airlines and automobile manufacturers are extremely cyclical, and have historically scored an ‘E’ rating because they follow a boom-or-bust like cycle. High operational leverage, meanwhile, means these businesses typically do well in good times, while are generally loss-makers during economic slowdowns or recessions.

‘In our view,’ Petersen added, ‘highly cyclical businesses are not well suited for a long-term buy and hold strategy, and rather require strong skills in timing the business cycle and trading. This is extremely hard to do, and very few people can do it on a consistent basis.’

As investing is about improving the odds of being right, the Fund has historically had a large allocation toward defensive stocks, holding around 30-50 stocks at any time with strong allocations to US, French, Japanese and Swiss companies. Meanwhile, consumer staples has been the largest allocation by sector at around 50%, along with strong names in healthcare, communications services and industrials.

‘These are businesses with a high degree of repeat sales, low capital intensity and steady earnings, which can help protect investors from downside risks if or when they emerge,’ Petersen remarked. ‘If there’s a slowdown, we know these companies can continue to do well throughout the business cycle.

It is important to note, however, that solid downside protection can only be achieved by not overpaying for earnings stability ’

‘High earnings stability translates to a low risk premium, and vice-versa for low earnings stability’

Klaus Petersen

This focus on defensive stocks, risk management, and ‘winning by losing less’ has been consistent over time too. Since inception of the Strategy around two decades ago, it has achieved an upside capture of 84% and a downside capture of 50% (in Euros, as at 31 July 2019), and has also performed strongly during difficult years including after the dot-com crash and the Global Financial Crisis. More recently in the fourth quarter of 2018, strong downside protection enabled the Strategy to end the year up, even as the broad market (MSCI World) finished down in Euros, further highlighting the utility of the team’s proprietary view on risk.

‘It’s not about stock price volatility,’ Hansen added. ‘It’s really all about earnings stability – that’s what’s important over the long-term. We are constantly searching the market to identify opportunities, and oftentimes it is the behaviour of myopic investors that presents us with the greatest opportunities. If we like a business and believe it has strong fundamentals but it misses an earnings quarter or two and gets downgraded, we view that as an opportunity. Overall, accurate analysis really requires a very strong understanding of the business and industry, and success is closely connected to the willingness of investing for the long-term.’

ESG – AN INTEGRATED PART OF RISK MANAGEMENT

Meanwhile, environmental, social and governance (ESG) has been, and continues to be, a focus for the team who pay close attention to any ESG risks the Fund’s holdings are likely to face – a process that’s becoming more and more important as ESG becomes mainstream.

‘In today’s social media world, where information can very quickly become public knowledge, companies’ top-line can be impacted almost instantly,’ Hansen explained.’

He added: ‘That’s why we have such a big focus on ESG, and employ a specialist in-house analyst. We were early signatories of the UNPRI principles back in 2010, when it was still in its infancy, but to us it’s about risk management. We don’t specifically exclude companies based on their ESG score, though a lower score could certainly lead to a higher risk premium when we value a company.’

THE DEMONSTRATED VALUE OF PATIENCE AND DISCIPLINE

This tried and tested approach, which involves over 20 years’ experience of being patient and disciplined, has certainly paid off for the team. Not only has the Strategy delivered strong performance, it has also outperformed the MSCI World Index over five, 10 and 20-years, and the Fund has been a top quartile Citywire performer over five years – a period where investors have piled into in-favour growth and momentum stocks [1].

‘We haven’t found the holy grail,’ Petersen conceded. ‘But we have built a solid low-risk strategy. Investors compare us to a minimum volatility strategy; we’ve actually had similar downside protection, but far more upside capture. This demonstrates that our focus on value and quality – and not just on volatility – can be successful over the long-term. And particularly during periods of uncertainty. Ultimately we don’t think of ourselves as being necessarily smarter, but certainly more patient and disciplined.’

‘If there’s a slowdown, we know these companies can continue to do well throughout the business cycle’

Klaus Petersen

GLOBAL EQUITY

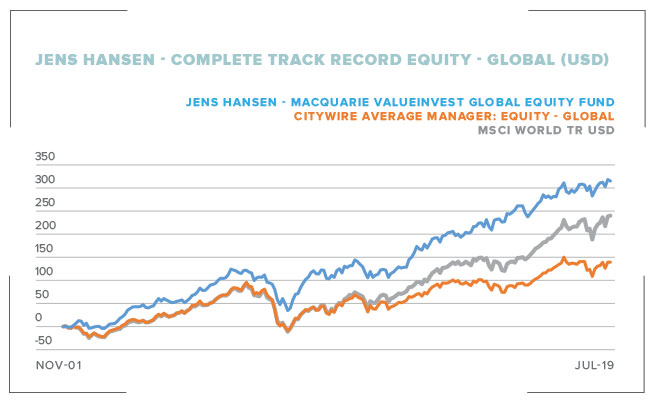

Over Jens Hansen’s career in global equities he has comfortably outperformed the Index and the average manager. He was particularly impressive during the credit crisis. Over three years until the end of March ’09 he was 75/704 managers worldwide, helped by the fact that he had a maximum drawdown in the 96th percentile.

The Macquarie ValueInvest Global Equity Strategy is managed via a collaborative team-based approach by four experienced portfolio managers: Jens Hansen (2001), Claus Juul (2004), Klaus Petersen (2006), and Åsa Annerstedt (2013).

SOURCE: Citywire Discovery/Lipper, as at 31.07.2019. Performance is based on total return in USD calculated gross of tax, net of fees, bid to bid, ignoring the effect of initial charges and with income reinvested at the ex-dividend date. Average manager is based upon the managers tracked Globally in Citywire’s Equity – Global sector.

Past performance does not guarantee future results.

The post credit crisis has not been an easy time to be a global equity manager, with the sustained rise of the US and technology in indices hampering investors’ ability to add value. Macquarie’s Hansen has managed to stay towards the top of the peer group during this time, with upper fourth decile returns over 10 years and upper third decile gains over the past three years, as can be seen by his position in the upper right hand quadrant of the graphic.

SOURCE: Citywire Discovery, as at 31.07.2019. Total Return percentiles are calculated in USD gross of tax, net of fees, bid to bid, ignoring the effect of initial charges and with income reinvested at the ex-dividend date. Peer group rankings are based on managers tracked by Citywire globally. Market share data based on total assets under management by managers tracked by Citywire.

FUND MANAGER HOT-SEAT

Q&A with Jens Hansen and Klaus Petersen

FUND MANAGER HOT-SEAT

Q&A with Jens Hansen and Klaus Petersen

Can you describe your investment approach, and explain why you believe patience is underrated?

Jens Hansen: We approach investing with patience and discipline. Our main belief is that long-term capital preservation and wealth accumulation are best achieved through buying quality businesses at attractive valuations, and then waiting until the fundamentals and earnings assert themselves.

The hallmarks of quality include profitability, earnings stability, low debt, and efficient use of assets – return on capital is a great indicator of how well a business is managed. Typically, this means we invest in very strong and stable businesses that can reinvest earnings at attractive returns and grow their potential over time. They might not dominate the headlines, but their returns are often very strong over time, and so we’re happy to avoid the noise.

In order to really compound wealth and maintain conviction in an approach, patience is key. This is something most investors lack; it’s often said that the hardest part of investing is doing nothing, and we agree. So while we monitor and track hundreds of companies, and particularly those in our portfolio, if we have high conviction in a stock, we don’t tend to get too swayed by short-term swings.

It’s incredibly hard to find an ‘edge’ in investing. What we’ve found over time though, is that a tried and tested approach of being patient and disciplined can help outperform the market over time. Fortunately, the approach has worked for us over the past 20 years.

What are the benefits of investing in ‘boring’ companies?

Klaus Petersen: I don’t know why people get the impression that investing should be exciting – it takes years, and a lot of patience. I think the stunning run of some companies, such as the FAANGs (Facebook, Amazon, Apple, Netflix, Google), has tempted some investors into thinking they can quickly grow wealth by trading or investing in just a few companies, but that’s not generally what happens.

It is an intriguing investment strategy; trying to accelerate wealth creation by picking the next Amazon or Google. Bear in mind that before the IT bubble burst we talked about finding the next Nokia. In hindsight, picking the winners is easy, but in practice it is like finding the proverbial needle in the haystack, and the attempt will undoubtedly lead to many failed investments and potentially large losses. In our view, it is better to invest when businesses are more mature and stable, and less of a lottery ticket.

Growth is good, and is the engine of an economy. We don´t deny that some of today´s fastest-growing companies, many of them within the technology sector, are great businesses, but in our experience investors tend to extrapolate high growth for too long which leads to overshooting.

So, the main benefit of investing in a broad portfolio of defensive companies, typically rated A and B according to our risk classification is that, although they tend to be mature and might not be growing at a high rate, they are still growing, and their earnings are predictable. In our experience, business models that are inherently more stable, generating solid returns on capital and producing excess cash after investing that can be returned to shareholders, are more likely to be good long-term investments.

And while these companies can often be neglected in big bull markets, such as that over the last few years, they tend to fare very well in more challenging environments or recessions because they aren’t so sensitive to the business cycle. That means they tend to do better over the entire cycle – and consequentially so has the Fund. The Strategy has outperformed the MSCI World Index since inception, and it’s also done very well in down years such as 2008. [2]

Where do you see the best opportunities?

Jens Hansen: Historically we have always had a large allocation to defensive stocks. We like businesses with low capital intensity and a steady earnings stream which can protect on the downside, particularly as they are less exposed to turns in the business cycle.

In the fourth quarter of 2018 these stocks became more popular, especially amongst investors wanting to stay invested, so that’s certainly been a tailwind for some of our holdings.

In terms of the sectors we’re invested in, it’s almost entirely driven by our fundamental bottom-up research. We don’t take macroeconomic views, because we believe trying to time the market is incredibly tough; we’d rather invest in companies that are less exposed to the business cycle in the first place.

So, what does the portfolio look like? Currently, we don’t have any investments in five of the 11 main sectors, including information technology, energy, utilities, real estate and financials. Simply from a bottom-up perspective we haven’t been able to find any tech companies; we identify a lot of quality, and these businesses can be very stable, but valuations are rich or fair given their strong businesses models.

Typically therefore we invest in a lot of consumer staples and healthcare companies in the US, France, Switzerland, Japan, and the United Kingdom.

These are companies in areas like packaged foods and meats, pharmaceuticals, food retail, and household products. What we like about them is they’re mature companies with excellent business models, strong earnings pipelines, sustainable competitive advantages, and proven resilience. Almost all of our top holdings for instance, are rated A or B – those with the highest earnings stability.

Ultimately what this means is that we have built a very robust portfolio with an ability to capture most of the upside in equities rallies, while simultaneously minimising a lot of the downside.

Can you provide some insight into your team?

Klaus Petersen: We’re a highly experienced and tightknit team working out of Luxembourg. Our four portfolio managers, including Jens and myself, have long track records in investing. I have over 34 years of industry experience, including 21 years as a portfolio manager, while Jens has slightly more overall experience. Meanwhile, we’ve both been managing this Fund together for the past 13 years, over which time it has achieved strong performance.

Aside from our experience and team stability, our collaborative approach has certainly helped too. All of the portfolio managers work as generalists and analysts, and we share the responsibility for company research – which is a very different approach compared to many other firms.

We’re always talking about different ideas and questioning each other’s calls or convictions. The team use a comprehensive and proprietary screening tool as the primary idea generator, and when we come across investment opportunities that meet our quality and value hurdles, one of our portfolio managers will conduct thorough research and number crunching to write the investment thesis.

Before discussing the investment case, we assign a second portfolio manager as devil´s advocate to identify weaknesses and risks in the case. Diversity of thought is important and it’s key to hear as many different viewpoints as possible, and not become biased in your own individual research or thinking. So having a small, cooperative group has been highly beneficial.

To find out more visit the Macquarie Investment Management website at macquarieIM.com.

[1] The Strategy refers to the Macquarie ValueInvest Global Equity Strategy and has delivered 13.2%pa, 13.4%pa and 9.9%pa (gross of fees) over the 5, 10 and 20 years to 31 July 2019 (Euros) with the MSCI World Index delivering 11.2%pa, 12.7%pa and 4.6%pa over the same periods. The Fund refers to the Macquarie ValueInvest Global Equity Fund and was a top quartile Citywire performer for 5 years from July 2014 to July 2019 according to Citywire Discovery/Lipper data as at 31st July 2019.

[2] The Macquarie ValueInvest Global Equity Strategy has delivered 10.72%pa (gross of fees) since inception on 31 July 1998.

This information is confidential and intended for the audiences as indicated. It is not to be distributed to, or disclosed to retail investors.

The views expressed represent the Investment team’s as of the date indicated, and should not be considered a recommendation to buy, hold, or sell any security, and should not be relied on as research or investment advice. Views are subject to change without notice.

This document has been created solely for initial general information purposes only. The information in this document is not, and should not be construed as, an advertisement, an invitation, an offer, a solicitation of an offer or a recommendation to participate in any investment strategy or take any other action, including to buy or sell any product or security or offer any banking or financial service or facility in any jurisdiction where it would be unlawful to do so. The information presented is not intended and should not be construed to be a presentation of information for any pooled vehicle including U.S. mutual funds. This document has been prepared without taking into account any person’s objectives, financial situation or needs. Recipients should not construe the contents of this document as financial, investment or other advice. It should not be relied on in making any investment decision.

Future results are impossible to predict. This document contains opinions, conclusions, estimates and other forward-looking statements which are, by their very nature, subject to various risks and uncertainties. Actual events or results may differ materially, positively or negatively, from those reflected or contemplated in such forward-looking statements. Past performance is not a reliable indicator of future performance. Investing involves risk including the possible loss of principal.

This document does not contain all the information necessary to fully evaluate any investment program, and reliance should not be placed on the contents of this document. Any decision with respect to any investment program referred to herein should be made based solely upon appropriate due diligence by the prospective investor. The investment capabilities described herein involve risks due, among other things, to the nature of the underlying investments. All examples herein are for illustrative purposes only and there can be no assurance that any particular investment objective will be realized or any investment strategy seeking to achieve such objective will be successful.

No representation or warranty, express or implied, is made as to the accuracy or completeness of the information, opinions and conclusions contained in this document. In preparing this document, reliance has been placed, without independent verification, on the accuracy and completeness of all information available from external sources.

To the maximum extent permitted by law, none of the entities under Macquarie Investment Management nor any other member of the Macquarie Group nor their directors, employees or agents accept any liability for any loss arising from the use of this document, its contents or otherwise arising in connection with it.

Other than Macquarie Bank Limited (MBL), none of the entities noted in this document are authorised deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of MBL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of these entities, unless noted otherwise.

The following investment advisers form part of Macquarie Group’s investment management business, Macquarie Investment Management: Macquarie Investment Management Business Trust, Macquarie Funds Management Hong Kong Limited, Macquarie Investment Management Austria Kapitalanlage AG, Macquarie Investment Management Global Limited, Macquarie Investment Management Europe Limited, Macquarie Capital Investment Management LLC, and Macquarie Investment Management Europe S.A.

The Strategy is subject to the following risks:

· The value of shares may fall as well as rise, and you may not receive back the amount invested.

· International investments may involve risk of capital loss from unfavourable fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations.

· The market for investments in emerging market countries may be less developed and it may be difficult for the fund to sell its investments in such markets. Investing in emerging markets can be riskier than investing in established markets due to increased volatility and lower trading volume.

· As a class, equities carry higher risks than bonds or money market instruments.

· If the strategy focuses on a single geographical area (Japan) there’s an increased risk that local political and economic conditions could adversely affect the performance of the strategy.

· Investing in small and/or medium-sized companies typically exhibit greater risk and higher volatility than larger, more established companies.

International risk. International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations.

Healthcare companies risk. Narrowly focused investments may exhibit higher volatility than investments in multiple industry sectors. Healthcare companies are subject to extensive government regulation and their profitability can be affected by restrictions on government reimbursement for medical expenses, rising costs of medical products and services, pricing pressure, and malpractice or other litigation.

For recipients in the European Economic Area, this document is a financial promotion distributed by Macquarie Investment Management Europe Limited (MIMEL) and Macquarie Investment Management Europe S.A. (MIME SA) to Professional Clients or Eligible Counterparties only, as defined in the Markets in Financial Instruments Directive 2014/65/EU. This document is not intended for distribution to Retail Clients. MIMEL is authorised and regulated by the Financial Conduct Authority. MIMEL is incorporated and registered in England and Wales (Company No. 09612439, Firm Reference No. 733534). The registered office of MIMEL is Ropemaker Place, 28 Ropemaker Street, London, EC2Y 9HD. MIME SA is authorised and regulated by the Commission de Surveillance du Secteur Financier. MIME SA is incorporated and registered in Luxembourg (Company No. B62793). The registered office of MIME SA is Villa Macquarie, 10a, Boulevard Joseph II, Luxembourg L-1840, Grand Duchy of Luxembourg.

This document has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research.

For recipients in Switzerland, this document is distributed by Macquarie Investment Management Switzerland GmbH. In Switzerland this document is directed only at qualified investors (the “Qualified Investors”), as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended (“CISA”) and its implementing ordinance.

For recipients in Australia, this document is provided by Macquarie Investment Management Global Limited (ABN 90 086 159 060 Australian Financial Services Licence 237843) solely for general informational purposes. This document does not constitute a recommendation to acquire, an invitation to apply for, an offer to apply for or buy, an offer to arrange the issue or sale of, or an offer for issue or sale of, any securities in Australia. This document has been prepared, and is only intended, for ‘wholesale clients’ as defined in section 761G of the Corporations Act and applicable regulations only and not to any other persons. This document does not constitute or involve a recommendation to acquire, an offer or invitation for issue or sale, an offer or invitation to arrange the issue or sale, or an issue or sale, of interests to a ‘retail client’ (as defined in section 761G of the Corporations Act and applicable regulations) in Australia.

For recipients in PRC, Macquarie is not an authorized securities firm or bank in mainland China and does not conduct securities or banking business in mainland China.

For recipients in Hong Kong, this document is provided by Macquarie Funds Management Hong Kong Ltd (CE No. AGZ772) (“MFMHK”), a company licensed by the Securities and Futures Commission (“SFC”), to professional investors only for the purpose of giving general information. The information contained in this document has not been approved or reviewed by the SFC and is provided on a strictly confidential basis for your benefit only and must not be disclosed to any other party without MFMHK’s prior written consent. If you are not the intended recipient you are not authorised to use this information in any way.

For recipients in Korea, this document is provided at the specific request of the recipient who is a professional investor as specified under Article 101(2) of the Presidential Decree of the Financial Investment Services and Capital Markets Act (“Act”) without any solicitation by Macquarie. This document may not be distributed, either directly or indirectly, to others in Korea. The products and services have not been registered under the Act, and none of the interests may be offered, sold or delivered, or offered or sold to any person for re-offering or resale, directly or indirectly, in Korea or to any resident of Korea except pursuant to applicable laws and regulations of Korea.

For recipients in Malaysia, Taiwan, The Philippines, Indonesia, this document does not and is not intended to constitute an invitation or an offer for purchase or subscription of securities, units of collective investments schemes or commodities, or any interests in any index thereof. The information in this document is prepared and only intended for professional investors.

For recipients in Thailand, this document is provided to Institutional Investors only for the purpose of giving general information. The information contained is provided on a strictly confidential basis for the intended recipient’s benefit only. If you are not the intended recipient, you are not authorised to use this information in any way. The contents of this information have not been reviewed by any regulatory authority. The transmission or distribution of this document by the intended recipient is unauthorised and may contravene local securities legislation.

For recipients in Singapore, the Strategies which are the subject of this document do not relate to a collective investment scheme which is authorised under section 286 of the Securities and Futures Act, Chapter 289 of Singapore (“SFA”) or recognised under section 287 of the SFA. The Strategies are not authorised or recognised by the Monetary Authority of Singapore and shares are not allowed to be offered to the retail public. This document may not be distributed, either directly or indirectly, to persons in Singapore other than (i) to an institutional investor under Section 304 of the SFA, (ii) to a relevant person pursuant to Section 305(1), or any person pursuant to Section 305(2), and in accordance with the conditions specified in Section 305 of the SFA, or (iii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA. Each of this document and any other document or material issued in connection with the document is not a prospectus as defined in the SFA. Accordingly, statutory liability under the SFA in relation to the content of prospectuses would not apply.

For recipients in Brunei, no prospectus relating to the strategies described in this document been delivered to, licensed or permitted by the Autoriti Monetari Brunei Darussalam as designated under the Brunei Darussalam Mutual Funds Order 2001, nor has it been registered with the Registrar of Companies. This document must not be distributed or redistributed to and may not be relied upon or used by any person in Brunei other than the person to whom it is directly communicated, (i) in accordance with the conditions of section 21(3) of the International Business Companies Order 2000, or (ii) whose business or part of whose business is in the buying and selling of shares within the meaning of section 308(4) of the Companies Act cap 39.

For recipients in Japan, this document is provided to Qualified Institutional Investors and other professional investors only by Macquarie Investment Management Advisers and/or its affiliate(s), which is/are supported by Macquarie Asset Management Japan Co., Ltd. (“MAMJ”), a Financial Instruments Business Operator: Director General of the Kanto Local Finance Bureau (Financial Instruments Business) No.2769 (Member of Japan Investment Advisers Association). MAMJ may distribute this document to non-professional investors by providing appropriate disclosure and taking any other action required to comply with the Financial Instruments and Exchange Act of Japan and with any other applicable laws and regulations of Japan.

Macquarie Group, its employees and officers may act in different, potentially conflicting, roles in providing the financial services referred to in this document. The Macquarie Group entities may from time to time act as trustee, administrator, registrar, custodian, investment manager or investment advisor, representative or otherwise for a product or may be otherwise involved in or with, other products and clients which have similar investment objectives to those of the products described herein. Due to the conflicting nature of these roles, the interests of Macquarie Group may from time to time be inconsistent with the Interests of investors. Macquarie Group entities may receive remuneration as a result of acting in these roles. Macquarie Group has conflict of interest policies which aim to manage conflicts of interest.

All third-party marks cited are the property of their respective owners.

© 2019 Macquarie Group Limited

957679

This communication is by Citywire Financial Publishers Ltd (“Citywire”) and is provided in Citywire’s capacity as financial journalists for general information and news purposes only. It is not (and is not intended to be) any form of advice, recommendation, representation, endorsement or arrangement by Citywire or an invitation to invest or an offer to buy, sell, underwrite or subscribe for any particular investment. In particular, the information provided will not address your particular circumstances, objectives and attitude towards risk.

Any opinions expressed by Citywire or its staff do not constitute a personal recommendation to you to buy, sell, underwrite or subscribe for any particular investment and should not be relied upon when making (or refraining from making) any investment decisions. In particular, the information and opinions provided by Citywire do not take into account your personal circumstances, objectives and attitude towards risk. Citywire uses information obtained primarily from sources believed to be reliable (such as company reports and financial reporting services) however Citywire cannot guarantee the accuracy of information provided, or that the information will be up-to-date or free from errors. Investors and prospective investors should not rely on any information or data provided by Citywire but should satisfy themselves of the accuracy and timeliness of any information or data before engaging in any investment activity. If in doubt about a particular investment decision an investor should consult a regulated investment advisor who specialises in that particular sector. Information includes but is not restricted to any video, article or guide content created or provided by Citywire.

For your information we would like to draw your attention to the following general investment warnings: The price of shares and investments and the income associated with them can go down as well as up, and investors may not get back the amount they invested. The spread between the bid and offer prices of securities can be significant in volatile market conditions, especially for smaller companies. Realisation of small investments may be relatively costly. Some investments are not suitable for unsophisticated or non-professional investors. Appropriate independent advice should be obtained before making any such decision to buy, sell, underwrite or subscribe for any investment and should take into account your circumstances and attitude to risk. Past performance is not necessarily a guide to future performance. Citywire Financial Publishers Ltd. is authorised and regulated by the Financial Conduct Authority (no: 222178).

Citywire Source is owned and operated by Citywire Financial Publishers Ltd (“Citywire”). Citywire is a company registered in England and Wales (company number 3828440), with registered office at 1st Floor, 87 Vauxhall Walk, London, SE11 5HJ and is authorised and regulated by the Financial Conduct Authority (no: 222178) to provide investment advice and is bound by its rules.

1. Intellectual Property Rights 1.1 We are the owner or licensee of all copyright, trademarks and other intellectual property rights in and to these works (including all information, data and graphics in them) (collectively referred to as “Content”). You acknowledge and agree that all copyright, trademarks and other intellectual property rights in this Content shall remain at all times vested in Citywire and /or its licensors. 1.2 This Content is protected by copyright laws and treaties around the world. All such rights are reserved. Images and videos used on our websites are © iStockphoto, Alamy, Thinkstock, Topfoto, Getty Images or Rex Features (among others). For credit information relating to specific images where not stated, please contact picturedesk@citywire.co.uk. 1.3 You must not copy, reproduce, modify, create derivative works from, transmit, distribute, publish, summarise, adapt, paraphrase or otherwise publicly display any Content without the specific written consent of a director of Citywire. This includes, but is not limited to, the use of Citywire content for any form of news aggregation service or for inclusion in services which summarise articles, the copying of any Fund manager data (career histories, profile, ratings, rankings etc) either manually or by automated means (“scraping”). Under no circumstance is Citywire content to be used in any commercial service.

2. Non-reliance 2.1 You agree that you are responsible for your own investment decisions and that you are responsible for assessing the suitability and accuracy of all information and for obtaining your own advice thereon. You recognise that any information given in this Content is not related to your particular circumstances. Circumstances vary and you should seek your own advice on the suitability to them of any investment or investment technique that may be mentioned. 2.2 The Fund manager performance analyses and ratings provided in this Content are the opinions of Citywire as at the date they are expressed and are not recommendations to purchase, hold or sell any investment or to make any investment decisions. Citywire’s opinions and analyses do not address the suitability of any investment for any specific purposes or requirements and should not be relied upon as the basis for any investment decision. 2.3 Persons who do not have professional experience in participating in unregulated collective investment schemes should not rely on material relating to such schemes. 2.4 Past performance of investments is not necessarily a guide to future performance. Prices of investments may fall as well as rise. 2.5 Persons associated with or employed by Citywire may hold positions or take positions in investments referred to in this publication. 2.6 Citywire Financial Publishers Ltd operate a policy of independence in relation to matters where the operators may have a material interest or conflict of interest.

3. Limited Warranty 3.1 Neither Citywire nor its employees assume any responsibility or liability for the accuracy or completeness of the information contained on our site. 3.2 You acknowledge and agree that any information that you receive through use of the site is provided “as is” and “as available” basis without representation or endorsement of any kind and is obtained at your own risk. 3.3 To the maximum extent permitted by law, Citywire excludes all representations, warranties, conditions or other terms, whether express or implied (by statute, common law, collaterally or otherwise) in relation to the site or otherwise in relation to any Content or Feed, including without limitation as to satisfactory quality, fitness for particular purpose, non-infringement, compatibility, accuracy, or completeness. 3.4 Notwithstanding any other provision in these Terms, nothing herein shall limit your rights as a consumer under English law.

4. Limitation of Liability To the maximum extent permitted by law, Citywire will not be liable in contract, tort (including negligence) or otherwise for any liability, damage or loss (whether direct, indirect, consequential, special or otherwise) incurred or suffered by you or any third party in connection with this Content, or in connection with the use, or results of the use of Content. Citywire does not limit liability for fraudulent misrepresentation or for death or personal injury arising from Citywire’s negligence.

5. Jurisdiction These Terms are governed by and shall be construed in accordance with the laws of England and the English courts shall have exclusive jurisdiction in the event of any dispute in connection with this Content or these Terms.